Governor Andrew Bailey takes questions from reporters, offering markets a clearer sense of how the central bank is thinking. His remarks follow the widely expected decision to keep the policy rate on hold at 3.75%.

This section below was published at 12:00 GMT to cover the Bank of England’s policy announcements and the initial market reaction.

At its February meeting, the Bank of England (BoE) held the policy rate at 3.75%, as markets had anticipated. The vote, however, exposed a split on the Monetary Policy Committee (MPC) as four members supported a 25-basis-point cut.

BoE policy statement takeaways

Andrew Bailey, Governor of the Bank of England, speaking after the February policy decision:

All going well, there should be scope for some further reduction in Bank Rate this year.

This does not mean I expect to cut Bank Rate at any particular meeting.

I expect CPI inflation to fall to around 2% in the spring, but we need to ensure it stays there.

Bank of England policy statement and Monetary Policy Report

- Policymakers voted 5–4 to hold Bank Rate at 3.75%, with Breeden, Dhingra, Ramsden and Taylor preferring a 25 basis point cut.

- The risk of greater inflation persistence has become less pronounced, although some downside risks from weaker demand and a looser labour market remain.

- Judgements around further policy easing will become a closer call.

- Bank Rate is likely to be reduced further.

Internal debate and guidance

- Greene, Lombardelli and Pill judged that a more prolonged period of policy restriction may be needed due to inflation risks.

- Bailey and Mann said they have greater confidence that rates will be cut, but that there is not yet enough evidence to act.

Updated forecasts and market pricing

- The forecast shows CPI returning to the 2% target in Q3 2026, earlier than previously expected.

- Inflation is projected at 1.7% in one year’s time and 1.8% in two years’ time, before returning to 2.0% in three years.

- Market rates imply slightly more near-term policy loosening than previously assumed, with the Bank Rate seen at 3.3% in Q4 2026.

- GDP growth is estimated at 0.2% QoQ in Q4 2025 and 0.3% QoQ in Q1 2026, with growth seen at 0.9% in 2026.

- Wage growth of around 3.25% is judged to be consistent with the 2% inflation target.

Market reaction to BoE policy announcements

Following the BoE event, GBP/USD keeps its bearish trend well in place, navigating the area of two-week lows in the 1.3560 region. Cable’s pullback also comes in tandem with the continuation of the upbeat mood in the US Dollar.

Pound Sterling Price Today

The table below shows the percentage change of British Pound (GBP) against listed major currencies today. British Pound was the strongest against the Japanese Yen.

| USD | EUR | GBP | JPY | CAD | AUD | NZD | CHF | |

|---|---|---|---|---|---|---|---|---|

| USD | 0.09% | 0.65% | 0.19% | 0.13% | 0.20% | 0.13% | 0.04% | |

| EUR | -0.09% | 0.57% | 0.09% | 0.04% | 0.11% | 0.05% | -0.05% | |

| GBP | -0.65% | -0.57% | -0.43% | -0.53% | -0.45% | -0.52% | -0.62% | |

| JPY | -0.19% | -0.09% | 0.43% | -0.07% | 0.02% | -0.07% | -0.15% | |

| CAD | -0.13% | -0.04% | 0.53% | 0.07% | 0.08% | 0.00% | -0.09% | |

| AUD | -0.20% | -0.11% | 0.45% | -0.02% | -0.08% | -0.07% | -0.17% | |

| NZD | -0.13% | -0.05% | 0.52% | 0.07% | -0.00% | 0.07% | -0.11% | |

| CHF | -0.04% | 0.05% | 0.62% | 0.15% | 0.09% | 0.17% | 0.11% |

The heat map shows percentage changes of major currencies against each other. The base currency is picked from the left column, while the quote currency is picked from the top row. For example, if you pick the British Pound from the left column and move along the horizontal line to the US Dollar, the percentage change displayed in the box will represent GBP (base)/USD (quote).

This section below was published as a preview of the Bank of England’s (BoE) interest rate decision at 07:00 GMT.

- The Bank of England is expected to keep its policy rate at 3.75%.

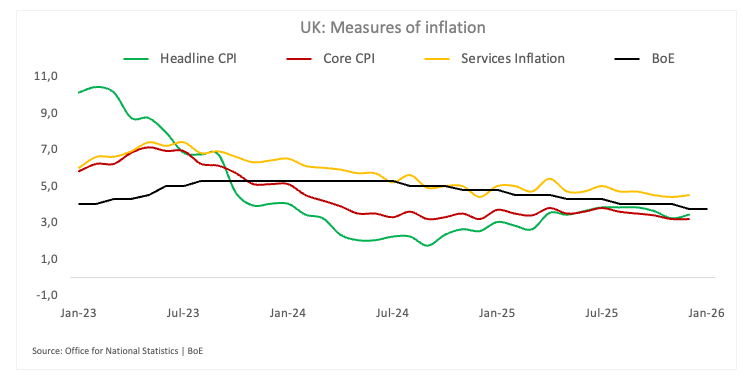

- UK inflation figures remain well above the BoE’s target.

- GBP/USD regains part of last week’s losses, hovering around 1.3700.

The Bank of England (BoE) will deliver its first monetary policy decision of 2026 on Thursday.

Most analysts think the ‘Old Lady’ will sit tight, keeping the base rate at 3.75% after the cut delivered back on December 18. Alongside the decision, the bank will also release the Minutes, which should shed a bit more light on how policymakers weighed the arguments around the table.

Markets are firmly priced for no move this time. However, the case for further easing hasn’t gone away, even if the BoE chooses to stay patient for now, as the UK economy struggles to gain any real traction and the fiscal backdrop continues to darken.

Inflation keeps running hot

The BoE’s December rate cut was a close-run thing. The 25 basis point move, which took the bank rate down to 3.75%, was carried by a narrow 5–4 vote. Indeed, members Breeden, Dhingra, Ramsden and Taylor all backed a cut, but it was Governor Bailey’s switch that proved decisive, underlining just how finely balanced the debate around further easing has become.

The message from the guidance was still cautiously dovish but noticeably more conditional. Policymakers stuck with the idea that rates are likely to move lower over time, describing a “gradual downward path”, while making it clear that each additional cut will be harder to justify. As policy drifts closer to neutral, the room for manoeuvre is shrinking, and the judgement calls are getting tougher.

The macro backdrop allows for further easing, but not with haste. Growth momentum has faded, with the economy expected to flatline in Q4, and inflation is projected to fall back more quickly in the near term, moving closer to the target by mid-2026. At the same time, lingering inflation bumps and a labour market that is only cooling slowly argue against flagging an aggressive cut cycle.

All told, December looks less like the start of a rush to ease and more like a careful recalibration. The Bank is still edging in an easier direction, but with rising caution as rates approach neutral and decisions become ever more dependent on incoming data.

According to the BoE’s Decision Maker Panel (DMP) published on January 8, businesses are growing a touch less punchy on pay, as firms now expect wages to rise by 3.7% over the 12 months from the final quarter of 2025, a shade lower than the pace they were expecting just a month earlier.

Additionally, companies are reducing their expectations for price increases in the upcoming year, which resulted in a 0.1 percentage point decrease to 3.6% in the three months to December.

And it’s not just wages and prices. Firms have also become slightly more cautious on hiring, with expectations for employment growth over the next year softening a little, according to the survey.

How will the BoE interest rate decision impact GBP/USD?

Many people expect the BoE will keep the reference rate at 3.75% when it makes its announcement on Thursday at 12:00 GMT.

The real focus will be on how the MPC votes, since a hold is already fully priced in. If the British Pound (GBP) moves in a way that isn’t expected, it could be because it suggests a change in how policymakers are getting ready for future decisions.

Pablo Piovano, Senior Analyst at FXStreet, notes that GBP/USD has come under fresh downside pressure soon after hitting yearly peaks near 1.3870 in late January, an area last traded in September 2021.

“Once Cable clears this level, it could then attempt a move to the September 2021 high at 1.3913 (September 14) ahead of the July 2021 peak at 1.3983 (July 30)”, Piovano adds.

On the other hand, Piovano says that “the critical 200-day SMA at 1.3421 emerges as the immediate contention in case sellers regain the upper hand prior to the 2026 floor at 1.3338 (January 19).”

“Meanwhile, the Relative Strength Index (RSI) near 61 suggests further gains remain in the pipeline in the near term, while the Average Directional Index (ADX) near 30 indicates a pretty strong trend,” he concludes.

Pound Sterling FAQs

The Pound Sterling (GBP) is the oldest currency in the world (886 AD) and the official currency of the United Kingdom. It is the fourth most traded unit for foreign exchange (FX) in the world, accounting for 12% of all transactions, averaging $630 billion a day, according to 2022 data.

Its key trading pairs are GBP/USD, also known as ‘Cable’, which accounts for 11% of FX, GBP/JPY, or the ‘Dragon’ as it is known by traders (3%), and EUR/GBP (2%). The Pound Sterling is issued by the Bank of England (BoE).

The single most important factor influencing the value of the Pound Sterling is monetary policy decided by the Bank of England. The BoE bases its decisions on whether it has achieved its primary goal of “price stability” – a steady inflation rate of around 2%. Its primary tool for achieving this is the adjustment of interest rates.

When inflation is too high, the BoE will try to rein it in by raising interest rates, making it more expensive for people and businesses to access credit. This is generally positive for GBP, as higher interest rates make the UK a more attractive place for global investors to park their money.

When inflation falls too low it is a sign economic growth is slowing. In this scenario, the BoE will consider lowering interest rates to cheapen credit so businesses will borrow more to invest in growth-generating projects.

Data releases gauge the health of the economy and can impact the value of the Pound Sterling. Indicators such as GDP, Manufacturing and Services PMIs, and employment can all influence the direction of the GBP.

A strong economy is good for Sterling. Not only does it attract more foreign investment but it may encourage the BoE to put up interest rates, which will directly strengthen GBP. Otherwise, if economic data is weak, the Pound Sterling is likely to fall.

Another significant data release for the Pound Sterling is the Trade Balance. This indicator measures the difference between what a country earns from its exports and what it spends on imports over a given period.

If a country produces highly sought-after exports, its currency will benefit purely from the extra demand created from foreign buyers seeking to purchase these goods. Therefore, a positive net Trade Balance strengthens a currency and vice versa for a negative balance.

Inflation FAQs

Inflation measures the rise in the price of a representative basket of goods and services. Headline inflation is usually expressed as a percentage change on a month-on-month (MoM) and year-on-year (YoY) basis. Core inflation excludes more volatile elements such as food and fuel which can fluctuate because of geopolitical and seasonal factors. Core inflation is the figure economists focus on and is the level targeted by central banks, which are mandated to keep inflation at a manageable level, usually around 2%.

The Consumer Price Index (CPI) measures the change in prices of a basket of goods and services over a period of time. It is usually expressed as a percentage change on a month-on-month (MoM) and year-on-year (YoY) basis. Core CPI is the figure targeted by central banks as it excludes volatile food and fuel inputs. When Core CPI rises above 2% it usually results in higher interest rates and vice versa when it falls below 2%. Since higher interest rates are positive for a currency, higher inflation usually results in a stronger currency. The opposite is true when inflation falls.

Although it may seem counter-intuitive, high inflation in a country pushes up the value of its currency and vice versa for lower inflation. This is because the central bank will normally raise interest rates to combat the higher inflation, which attract more global capital inflows from investors looking for a lucrative place to park their money.

Formerly, Gold was the asset investors turned to in times of high inflation because it preserved its value, and whilst investors will often still buy Gold for its safe-haven properties in times of extreme market turmoil, this is not the case most of the time. This is because when inflation is high, central banks will put up interest rates to combat it.

Higher interest rates are negative for Gold because they increase the opportunity-cost of holding Gold vis-a-vis an interest-bearing asset or placing the money in a cash deposit account. On the flipside, lower inflation tends to be positive for Gold as it brings interest rates down, making the bright metal a more viable investment alternative.